Business Sentiment Shows Early Signs of Stabilisation in Q4 2025, Firms Remain Cautiously Positioned for 2026

The Singapore Business Federation (SBF) today released findings from its National Business Survey 2025 – Q4 Business Sentiments Edition indicating early signs of stabilisation in business sentiments, as firms navigate persistent global cost and trade pressures while positioning for measured recovery.

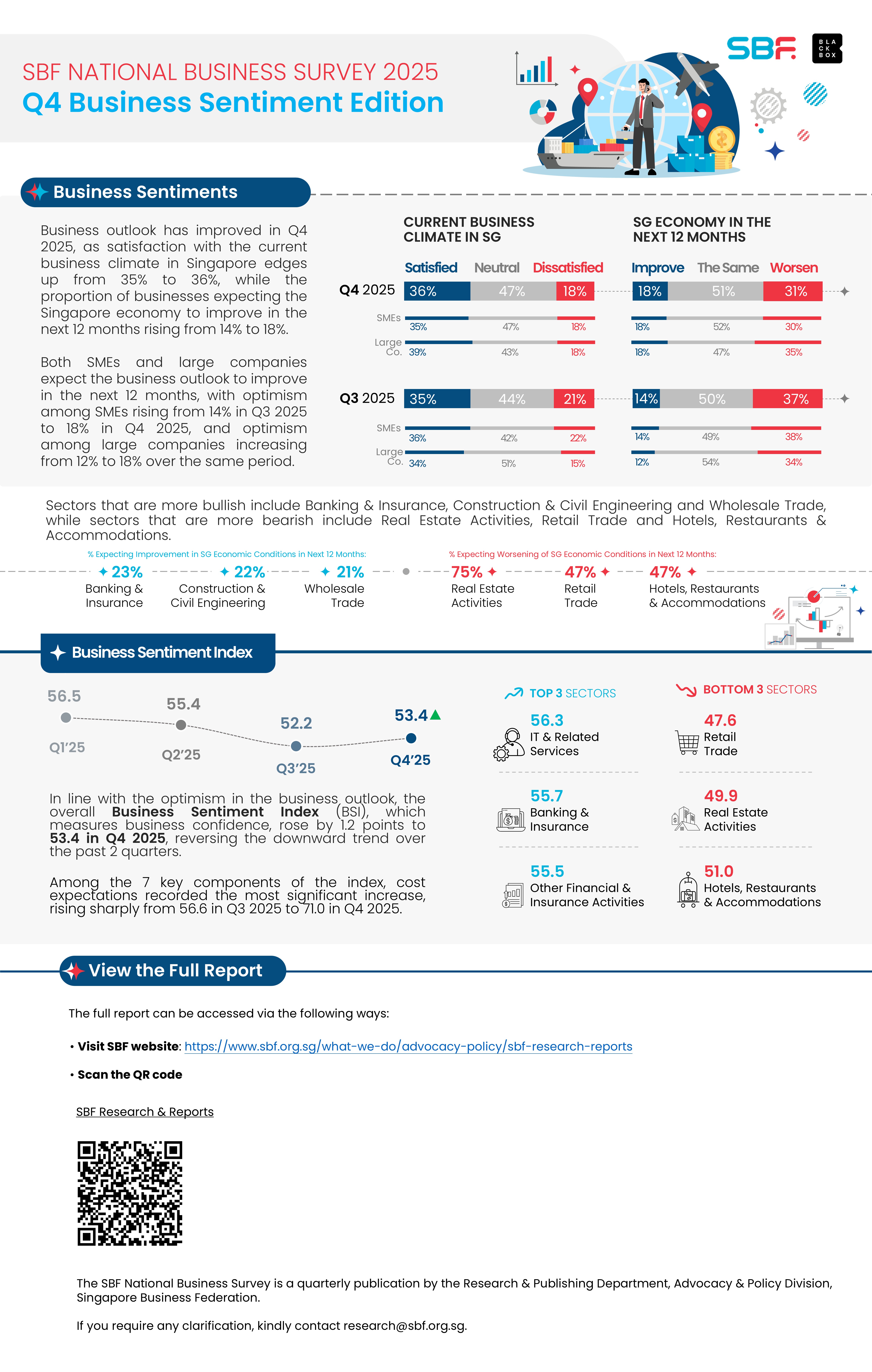

Overall business sentiment has turned cautiously positive, with the Business Sentiment Index (BSI) rising by 1.2 points to 53.4 in Q4 2025, breaking a six-month downward trend. This return to a neutral to slightly positive range aligns with Singapore’s strong Gross Domestic Product (GDP) growth in Q4 2025, suggesting macro conditions are stabilising after earlier volatility.1

Business outlook improved in Q4 2025, with satisfaction towards the current business climate in Singapore edging up from 35% to 36%, while the proportion of businesses expecting Singapore’s economy to improve over the next 12 months rose from 14% to 18%. Despite this improvement, most businesses remain cautious, with the majority anticipating no change in economic conditions (51%).

Key Findings

Sectoral Sentiment Remains Uneven Across Industries: The strongest improvement in overall sentiment was seen in the IT & Related Services sector, with the largest rebounds across multiple sub-indices. Banking & Insurance and Other Financial & Insurance Activities sectors also performed positively. Conversely, Retail Trade, Real Estate Activities, and Hotels, Restaurants & Accommodations remain the most challenged sectors.

Profitability Expectations Have Recovered: Profitability expectations improved from 48.5 to 52.1, reversing declines seen in Q2 and Q3 2025 across SMEs and large companies. The IT & Related Services sector recorded the strongest rebound, while Retail Trade, Education, and Administrative & Support Service Activities remain relatively less positive on profitability expectations.

Growth Confidence Is at Its Strongest Point in 2025: Growth confidence increased from 55.4 to 57.7, the highest level recorded in 2025. Gains were driven primarily by SMEs, while confidence among large companies remained stable. IT & Related Services, Other Service Activities, and Banking & Insurance registered the strongest sectoral improvements, while Retail Trade reported softer confidence.

Capacity Utilisation Is Rising, Signalling Emerging Pressure Points: Operational capacity utilisation rose from 55.2 to 57.9, supported by stronger year-end economic activity. Sectors such as Professional Services, IT & Related Services, and Hotels & Accommodations are beginning to see signs of capacity pressure, indicating potential constraints should growth accelerate.

Access To Financing Remains Stable, Not Easing: Access to financing remained steady at 54.7, indicating that financing conditions have not eased despite improved growth expectations. Large companies report comparatively better access than SMEs, while Retail Trade, Administrative & Support Services, and Hotels, Restaurants & Accommodations continue to experience the tightest financing conditions.

Cost Pressures Are the Dominant Near-Term Concern: Cost pressures emerged as a key near-term concern, with cost expectations rising sharply from 56.6 in Q3 2025 to 71.0 in Q4 2025, the most pronounced shift among BSI components. Most businesses anticipate higher costs over the next six months, particularly in sectors already facing tighter financing conditions such as Retail Trade and Administrative & Support Services, indicating that margin pressures may intensify even as demand conditions show signs of improvement.

Hiring Intentions Remain Cautious: Hiring expectations remained largely stable at 56.5, signalling that most businesses intend to maintain current workforce levels. Hiring sentiment is comparatively stronger in IT & Related Services, Professional Services, and Hotels, Restaurants & Accommodations, while Retail Trade, Real Estate, and Construction & Civil Engineering report weaker intentions.

Sentiment towards Government Support Is Stable but Uneven: Sentiment towards government policies moderated to 55.7, with large companies reporting a more pronounced decline. Sectoral sentiment is strongest in IT & Related Services and Banking & Insurance, while Retail Trade, Real Estate, and Hotels, Restaurants & Accommodations trail behind.

Mr Kok Ping Soon, Chief Executive Officer of SBF, said, “While business sentiment has shown signs of stabilisation in the fourth quarter, companies remain cautious. Improvements in growth confidence and profitability are being tempered by persistent cost pressures and ongoing tariff uncertainty in the US, leading many businesses to prioritise resilience and cost discipline over expansion. The escalation of conflict in the Middle East is also a concern for Singapore businesses because of its impact on global energy markets, shipping routes and business confidence. However, businesses shouldn’t wait for perfect clarity. SBF encourages companies to take a proactive approach by reviewing their supply chain resilience, managing costs and currency risks and maintaining close communication with customers and partners. Those who do will stay competitive. Businesses don’t have to navigate this alone — SBF is here to help firms build resilience, access support, and adapt confidently to this new trade environment.”

Annex A: SBF National Business Survey 2025 – Q4 Business Sentiments Edition Report

Annex B: SBF National Business Survey 2025 – Q4 Business Sentiments Edition Infographic

{kind=link}